Americana Restaurants (6015) Annual Report 2025: Cash Flow and High Capital Efficiency

Americana Restaurants operates as a large-scale regional franchise operator. The 2025 report reveals a business that generates high returns on capital by pairing iconic global brands with operational leverage. With revenue exceeding USD 2.51 billion and operating cash flow surging to USD 589 million, the platform routinely produces value far beyond its cost of capital.

What Does Americana Do?

Americana Restaurants International PLC (Tadawul: 6015 / ADX: AMR) is a leading pan-regional franchise operator. Present in 12 countries across the MENA region and Kazakhstan, the group manages a broad network of nearly 2,750 outlets representing major global brands like KFC, Pizza Hut, Hardee’s, Krispy Kreme, and Costa Coffee. (Note: While Americana trades in SAR on the Tadawul and AED on the ADX, it reports its financial results in USD).

The Major GCC segment is the primary driver of the business, generating USD 1.82 billion (73% of total revenue) and USD 215 million in segment profit. Other operational components, spanning the Lower Gulf and North Africa, add incremental scale but contribute significantly less to the bottom line, reflecting different competitive densities and currency dynamics.

The group operates under joint control structure. Adeptio AD Investments holds a 66.03% stake, an entity ultimately shared evenly between private interests (Mohamed Ali Rashed Alabbar) and a subsidiary of Saudi Arabia’s Public Investment Fund (PIF). The company has 8.42 billion shares outstanding globally across its dual listing.

Revenue & Earnings

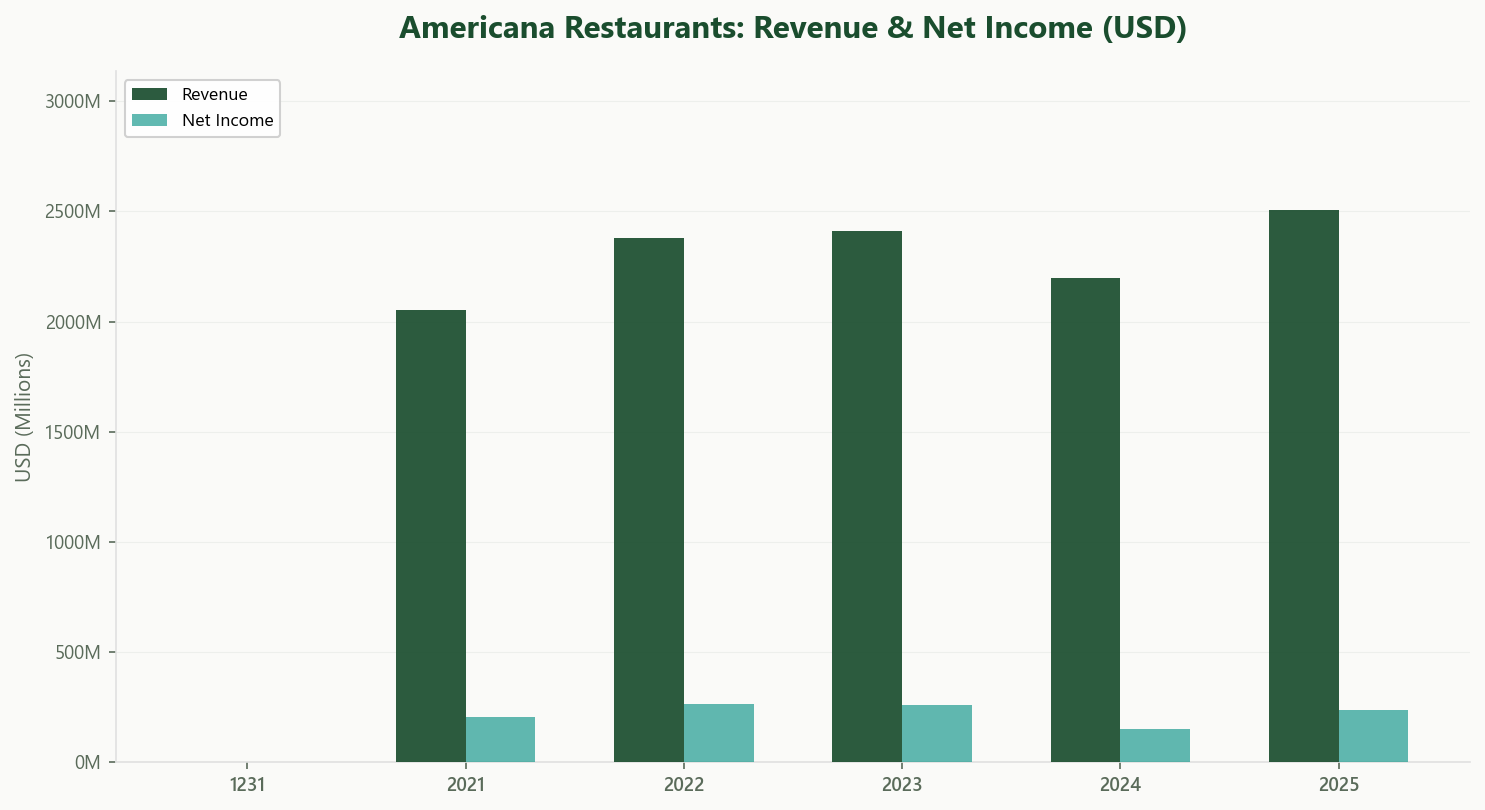

Top-line sales continue an consistent upward trajectory. Americana posted USD 2.51 billion in revenue for 2025, expanding from USD 2.20 billion in 2024.

The bottom line expanded alongside the top line. Net income reached USD 218.4 million (EPS of USD 0.026), an increase over the USD 151.4 million recorded the prior year. Structural operating leverage ensures that marginal revenue drops effectively to the bottom line without excessive incremental corporate overhead.

Operating profit (EBIT) stood at USD 282.7 million for the year. This operating cadence provides a fundamental margin of safety, absorbing regional volatility without jeopardizing corporate stability.

Despite the broad strength, the income statement absorbed a few non-cash impacts. Net non-recurring items included USD 5.56 million in impairment charges tied to property and right-of-use assets, and a modest net provision for slow-moving inventory at USD 2.66 million. Hyperinflationary dynamics contributed only a benign USD 1.05 million monetary loss, primarily isolated to regional exposures.

Profitability & Value Creation

Americana operates in a state of high capital efficiency. Historically generating an elite Return on Invested Capital (ROIC) averaging near 70.2%, the business generates substantial cash flow. With its Weighted Average Cost of Capital (WACC) hovering in the 7 to 8% range, the spread is significant. Very few operators in the region extract this much excess yield per unit of capital deployed.

The franchise model limits heavy direct capital intensity. Capital expenditures measured USD 94.8 million for the year, intentionally running below the hefty USD 307.0 million allocated to depreciation and amortization (which heavily features right-of-use lease amortization). This leaves significant capacity for cash distribution.

Segment margins heavily favor the mature markets. The Major GCC markets deliver robust absolute profit pools. Conversely, operations in the Lower Gulf and North Africa face tighter economics (reporting segment margins near 4% and 2.7% respectively).

Governance arrangements reflect the dual sovereign-private structure and are worth monitoring. The PIF and Mohamed Alabbar joint ownership channels substantial scale, but the group maintains deep operational links with affiliated entities. The company executed USD 59.4 million in raw material purchases from fellow subsidiaries, alongside USD 5.0 million in strategic advisory fees to a related entity. Furthermore, Americana consolidates specific joint ventures (like Bahrain and Kuwait Restaurants) despite holding only 40% voting equity, pointing to significant contractual entrenchment through exclusive management rights. These related-party transactions remain an integral part of the core supply chain.

Cash Flow & Balance Sheet

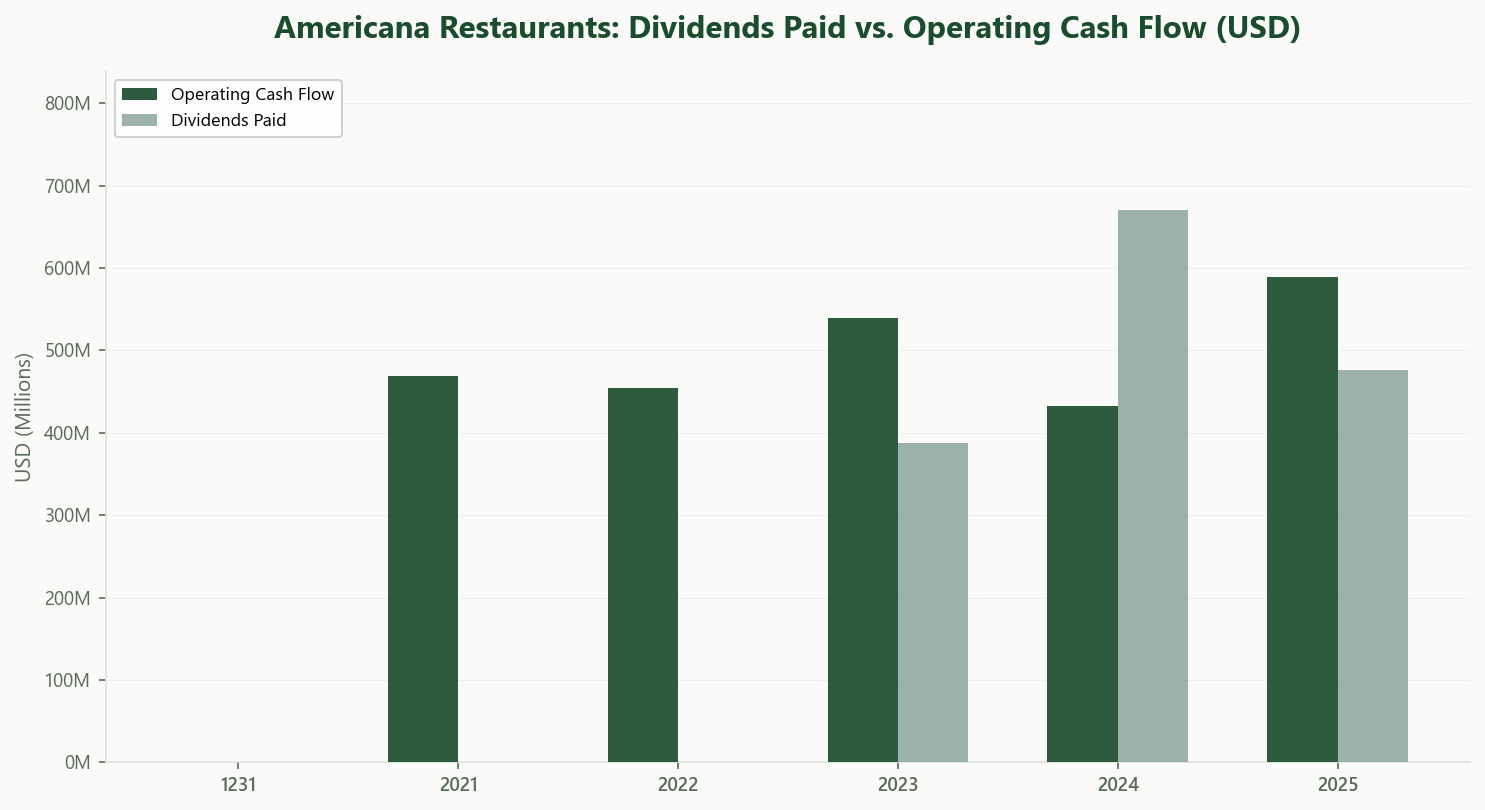

Cash conversion is a core strength for Americana. Operating cash flow reached USD 589.0 million in 2025, exceeding reported net income. This represents an efficient cash conversion cycle where favorable payable terms map against immediate retail cash collection.

Free cash flow remains robust. Subtracting moderate capex leaves roughly half a billion dollars in free cash available annually. This flow supports the group’s consistent dividend policy, having paid USD 127.4 million while declaring an additional USD 126.9 million by year-end.

The balance sheet carries no conventional bank debt. The equity base is capitalized with USD 394.4 million in total shareholder equity against USD 1.50 billion in assets (driven largely by USD 566 million in right-of-use franchise lease assets).

What looks like leverage is entirely lease obligations. Current finance leases stand at USD 189.5 million, while long-term lease liabilities make up USD 389.2 million. These represent the structural reality of retail footprints rather than financial risk.

Liquidity is tightly managed. The group holds USD 81.4 million in pure cash alongside USD 213.6 million in short-term investments, easily covering near-term cash liabilities when combined with the consistent monthly operational cash flows.

Valuation & What It Implies

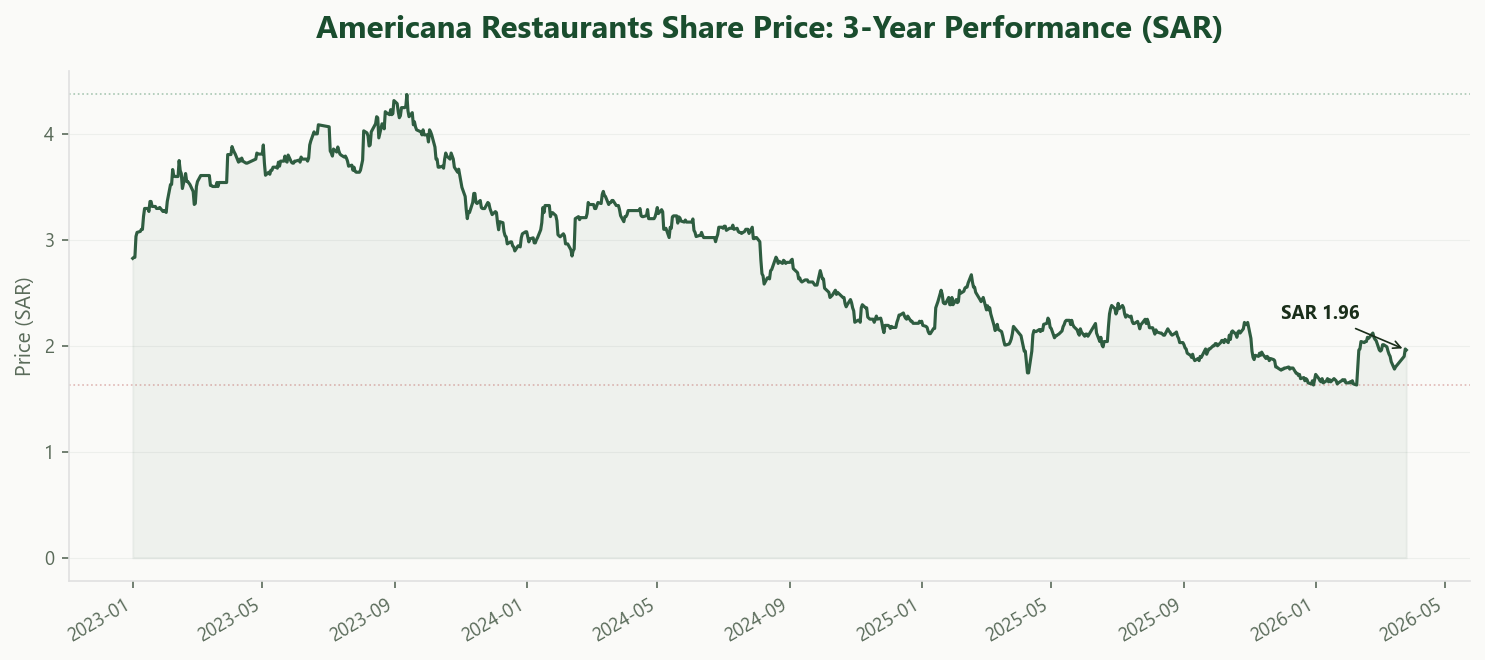

At the current Tadawul pricing near SAR 1.96 per share (approx. USD 4.4 billion implied market capitalization):

Given the 8.42 billion global shares outstanding across dual exchanges, the group commands a substantial market capitalization. Operating on an impressive P/E ratio multiple reflective of a premium consumer asset, the market expects cash yields to remain completely undisrupted.

Enterprise value tracks closely to market cap given the absence of traditional leverage, though capitalization of massive operating leases drives EV/EBITDA into the upper 20s. This is the price of admission for a highly defensive asset generating 70% structural returns on capital.

The bull case: Americana continues to utilize its substantial Major GCC free cash flow to fund steady unit additions while defending market share via digital investments and premium real estate locking. Yield-seeking investors remain anchored by the highly visible cash distributions.

The bear case: Currency fluctuations in frontier environments (like Egypt) bleed upwards, while aggregator competition compress margins across mature hubs. The valuation multiple is so demanding that any temporary stall in revenue momentum or operational cash flow conversion could compress shares significantly.

Takeaway

Americana is a clear example in utilizing a franchise model to extract high capital efficiency. Operating cash flows approaching USD 600 million coupled with a zero-bank-debt framework present a structurally fortified consumer business heavily anchored in Saudi Arabia and the UAE.

The primary considerations involve the concentrated reliance on the Major GCC segment to offset macro headwinds elsewhere, alongside the volume of related-party raw material procurement that funnels through the joint PIF-Alabbar superstructure.

Tadawul investors are paying a premium for this predictability and yield. The question remains: can Americana maintain the strong cash generation needed to sustain a premium multiple in a crowded retail landscape?

Explore Americana’s Full Profile

Usool Research tracks Americana’s financials, governance disclosures, valuation metrics, and more. Structured and updated from every filing.

Sign up free and explore the data.

Start Exploring →Look for value. Cut through the noise.

Disclaimer: This article is for informational and educational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any securities. The author and Usool Research may hold positions in securities discussed. Usool Research is not a licensed investment advisor. All data sourced from publicly available filings and the Usool Research platform.