Amiantit (2160) Annual Report 2025: Covenant Breaches and a Restructured Balance Sheet

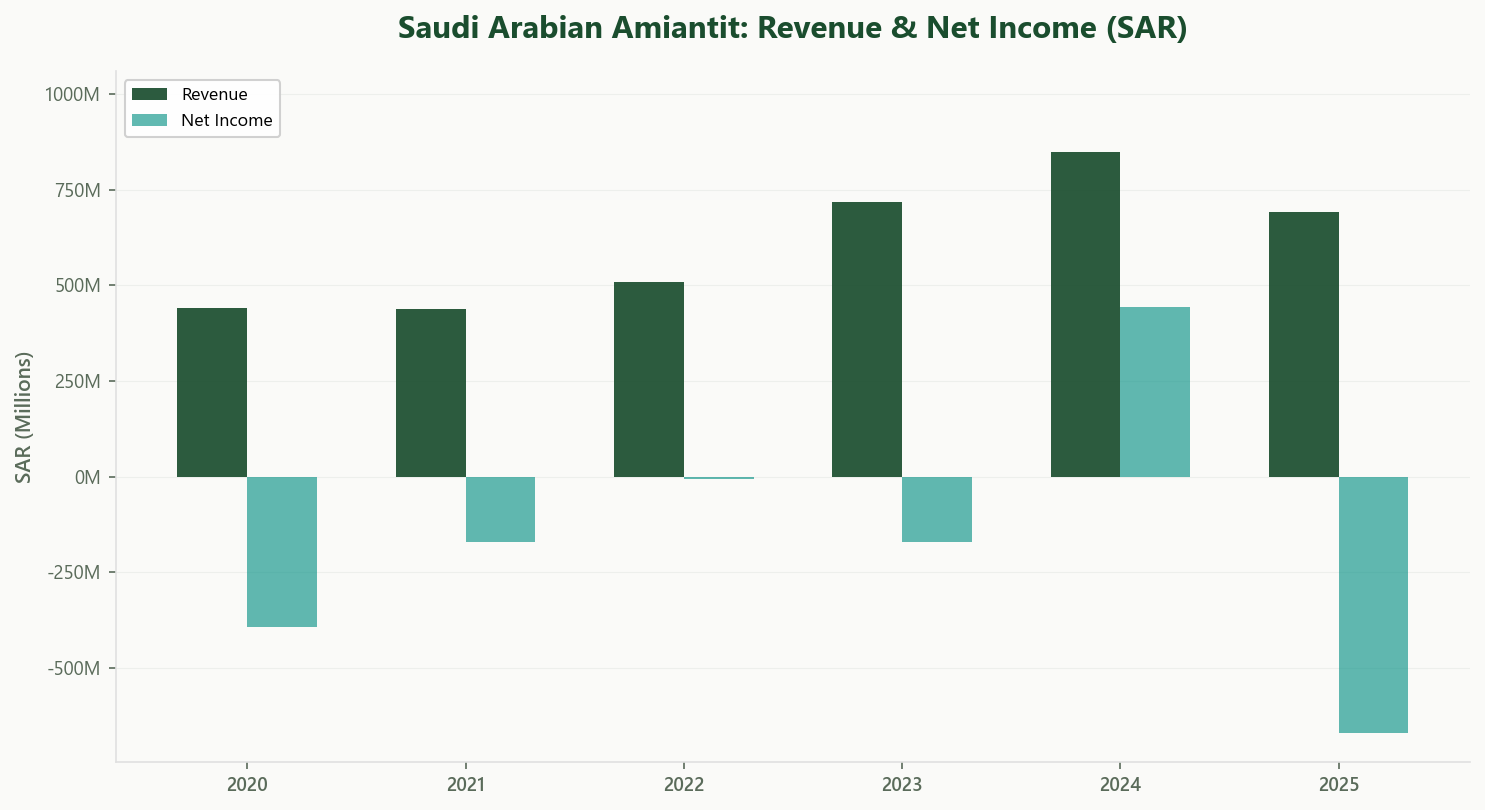

Saudi Arabian Amiantit Co. spent the last two years engineering a significant debt restructuring, settling over SAR 885 million in bank obligations. However, the core pipe manufacturing operations remain loss-making. With 2025 revenue at SAR 691.1 million and a net loss of SAR 671.9 million, breached financial covenants have shifted term loans back to current liabilities, testing the company’s fragile liquidity.

What Does Amiantit Do?

Saudi Arabian Amiantit Co. (Tadawul: 2160) is a capital goods manufacturer specializing in various types of pipes, related technological licensing, and water management services. The Group heavily relies on the Eastern and Central regions of Saudi Arabia, with corporate clientele composing over 98.4% of its revenue base.

The business operates via two primary segments. In 2025, Pipe Manufacturing and Technology generated the large majority of revenue at SAR 645.0 million, though it incurred a segment loss of SAR 47.9 million. The smaller Water Management segment generated SAR 92.4 million, posting a segment loss of SAR 38.0 million.

Amiantit operates with 44.51 million outstanding shares following a substantial SAR 346.5 million rights issue executed in 2025 aimed directly at repairing an insolvent capital structure.

Revenue & Earnings: Sales Decline and a Fading Turnaround Narrative

Top-line performance contracted in 2025, with revenue declining nearly 19% to SAR 691.1 million from SAR 848.3 million in 2024. The contraction reflects broader market compression in industrial capital expenditures and prolonged execution cycles in infrastructure contracting.

The bottom line in 2024 was primarily driven by non-recurring events. The company posted SAR 444.1 million in net income, driven entirely by a SAR 511.7 million gain on debt settlement and a SAR 71.8 million gain on the sale of a subsidiary. Strip those out and the structural weakness is clear.

In 2025, without those non-recurring items, net income reverted to SAR -671.9 million (EPS of SAR -15.09). EBIT came in at SAR -73.5 million, confirming that the core business is not yet self-funding.

Earnings were further burdened by balance sheet cleanups: a SAR 166.2 million write-down of contract assets and a SAR 37.7 million onerous contract provision, absorbing any underlying margin stabilization.

Profitability & Value Creation

The company continues to experience a decline in value creation. ROIC is consistently negative against a WACC in the 6 to 8% range. The business does not cover its cost of capital and remains reliant on external equity injections.

Capital intensity is tightly controlled, reflecting a focus on liquidity rather than capacity expansion. Capex in 2025 was minimal at SAR 8.1 million, sitting well below the ongoing depreciation and amortization run-rate of SAR 26.8 million.

Neither segment is profitable. Even on reduced asset bases, both Pipe Manufacturing and Water Management recorded operational losses—a structural mismatch between fixed overhead and actual contract throughput.

The balance sheet underwent material restructuring involving significant related-party support, worth monitoring. To settle SAR 572.7 million in liabilities, the company transferred 100% of its Amiwater subsidiary to an investment fund managed by an Alinma Bank affiliate. An ongoing judicial dispute over the ownership of a SAR 150 million land parcel in Jeddah—originally acquired from a related party—reflects legacy governance complexities and introduces additional asset risk. Collectively, these arrangements point to a business deeply reliant on external balance sheet relief.

Cash Flow & Balance Sheet

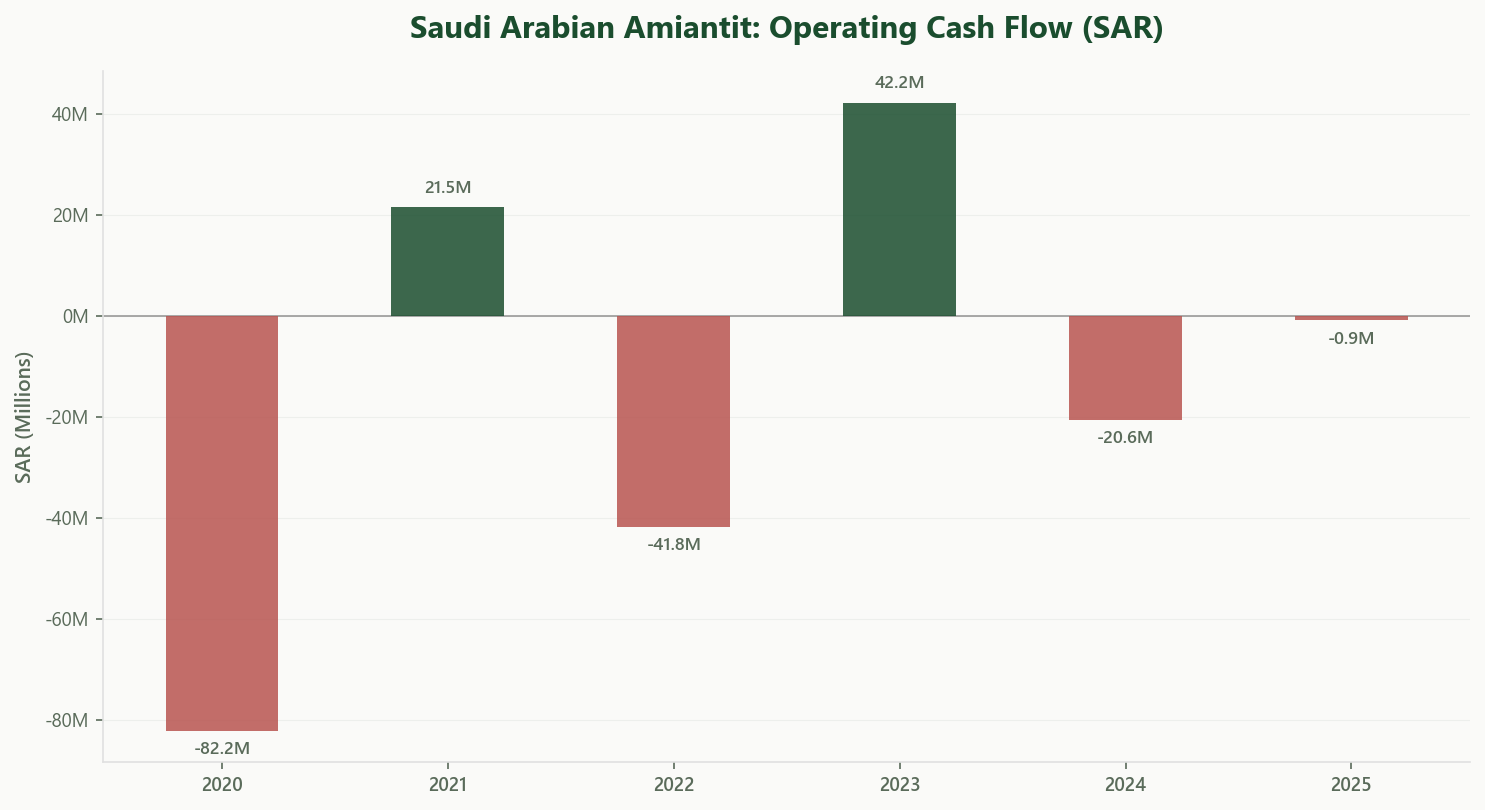

Cash generation remains structurally impaired. Operating cash flow in 2025 was marginally negative at SAR -0.85 million, tracking close to the SAR -20.6 million in 2024. The inability to generate internal cash remains the core bottleneck for recovery.

With no internally generated cash flow, the company is unable to distribute yields. Amiantit paid zero dividends in 2025 as all available liquidity is actively diverted toward creditor negotiations and operational survival.

Despite the restructuring, the balance sheet remains constrained. Shareholder equity stands at SAR 849.8 million, propped up by the SAR 346.5 million rights issue. Cash and equivalents: SAR 28.2 million.

The core risk centers on debt compliance. In 2025, Amiantit breached material financial covenants related to its credit facilities. Consequently, lenders now possess acceleration rights, forcing the company to reclassify SAR 207.5 million of long-term loans as short-term borrowings, sending its total current outstanding borrowings to SAR 228.4 million.

Tax liabilities pose an additional drag on capital. The group entered into an extended installment plan with ZATCA to settle SAR 277.7 million in legacy zakat dues spanning back to 2015, partially executing this via the assignment of claims against government entities.

Valuation & What It Implies

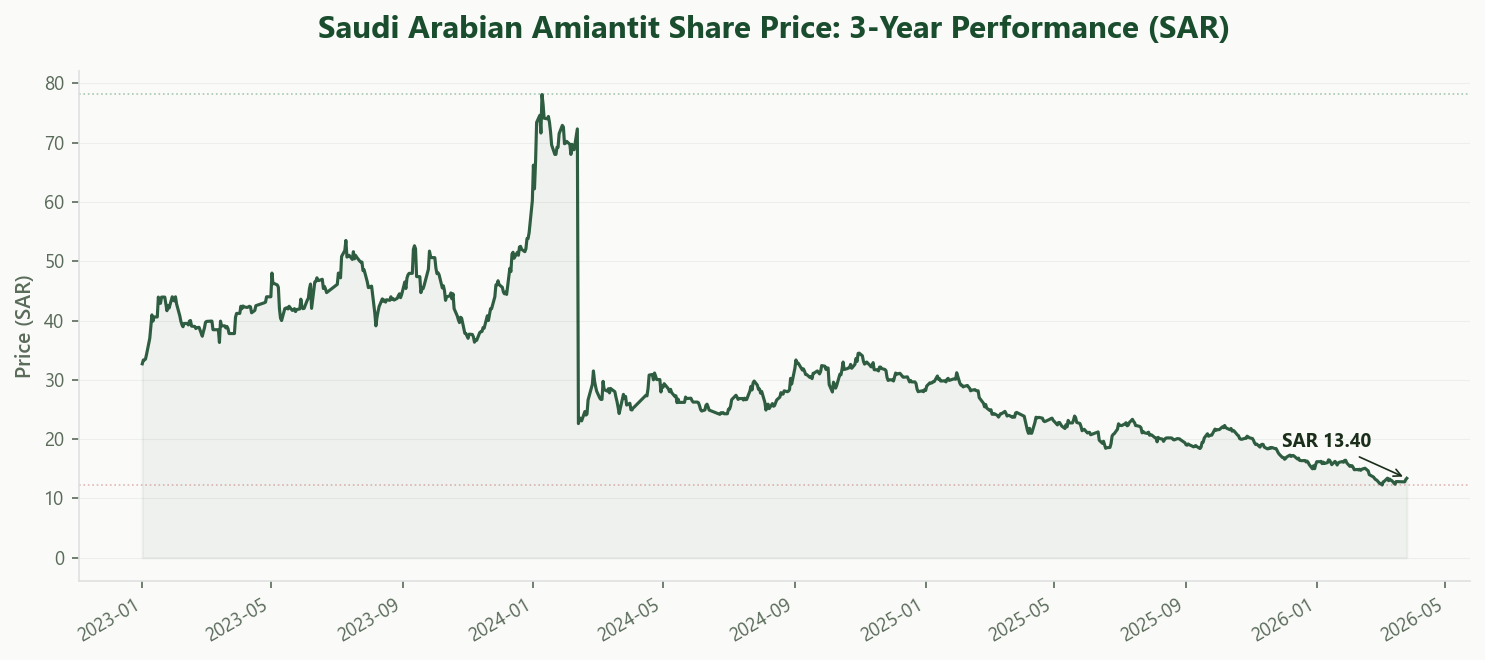

At the assumed anchor price of SAR 25.00 per share:

With 44.51 million shares outstanding, the implied market capitalization is roughly SAR 1.11 billion. Pricing an entity with negative operating cash flow, loss-making segments, and active covenant breaches requires a turnaround framework. Standard multiples like EV/EBITDA or P/E are not meaningful here.

Enterprise value is acutely sensitive to the near-term liquidity position. The forced reclassification of long-term debt into current liabilities amplifies short-term risk. The valuation debate hinges on whether management can renegotiate the breached covenants before full acceleration.

The bull case: Management successfully executed the forgiveness of significant bank debt in 2024 and recapitalized via the recent rights issue. If they can address the 2025 covenant breaches, the balance sheet resets, providing a clean slate to slowly transition the pipe manufacturing segment back into an operational surplus.

The bear case: The core operations remain unprofitable despite the restructured balance sheet. If Amiantit depletes the SAR 346 million rights issue proceeds before reaching operating profitability, the covenant breaches may trigger a liquidity crisis, potentially leading to further dilution upon existing shareholders.

Takeaway

Amiantit\'s recent performance is heavily characterized by financial restructuring. The balance sheet was materially restructured through debt forgiveness and a rights issue, yet the underlying business generated SAR 691.1 million in revenue at a full operating loss.

The focus now shifts from historical debt to the immediate covenant breaches. Acceleration risk on SAR 228.4 million in reclassified short-term debt is material, given a cash buffer of just SAR 28.2 million.

At an implied market cap of SAR 1.1 billion, equity investors are pricing a turnaround that has not yet materialized in the numbers. Is the debt restructuring the final hurdle, or a postponement of the underlying failure to generate positive cash flow?

Explore Amiantit’s Full Profile

Usool Research tracks Amiantit’s financials, governance disclosures, valuation metrics, and more. Structured and updated from every filing.

Sign up free and explore the data.

Start Exploring →Look for value. Cut through the noise.

Disclaimer: This article is for informational and educational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any securities. The author and Usool Research may hold positions in securities discussed. Usool Research is not a licensed investment advisor. All data sourced from publicly available filings and the Usool Research platform.