stc Group:

Annual Report

2025: Beyond the Record Headlines

stc group announced record revenues of SAR 77.8 billion and highlighted 12.5% net profit growth after excluding non-recurring items. These are strong results, but they only tell part of the story. Here's what the 2025 annual report shows and what the press release left out.

Revenue & Earnings: The Full Picture

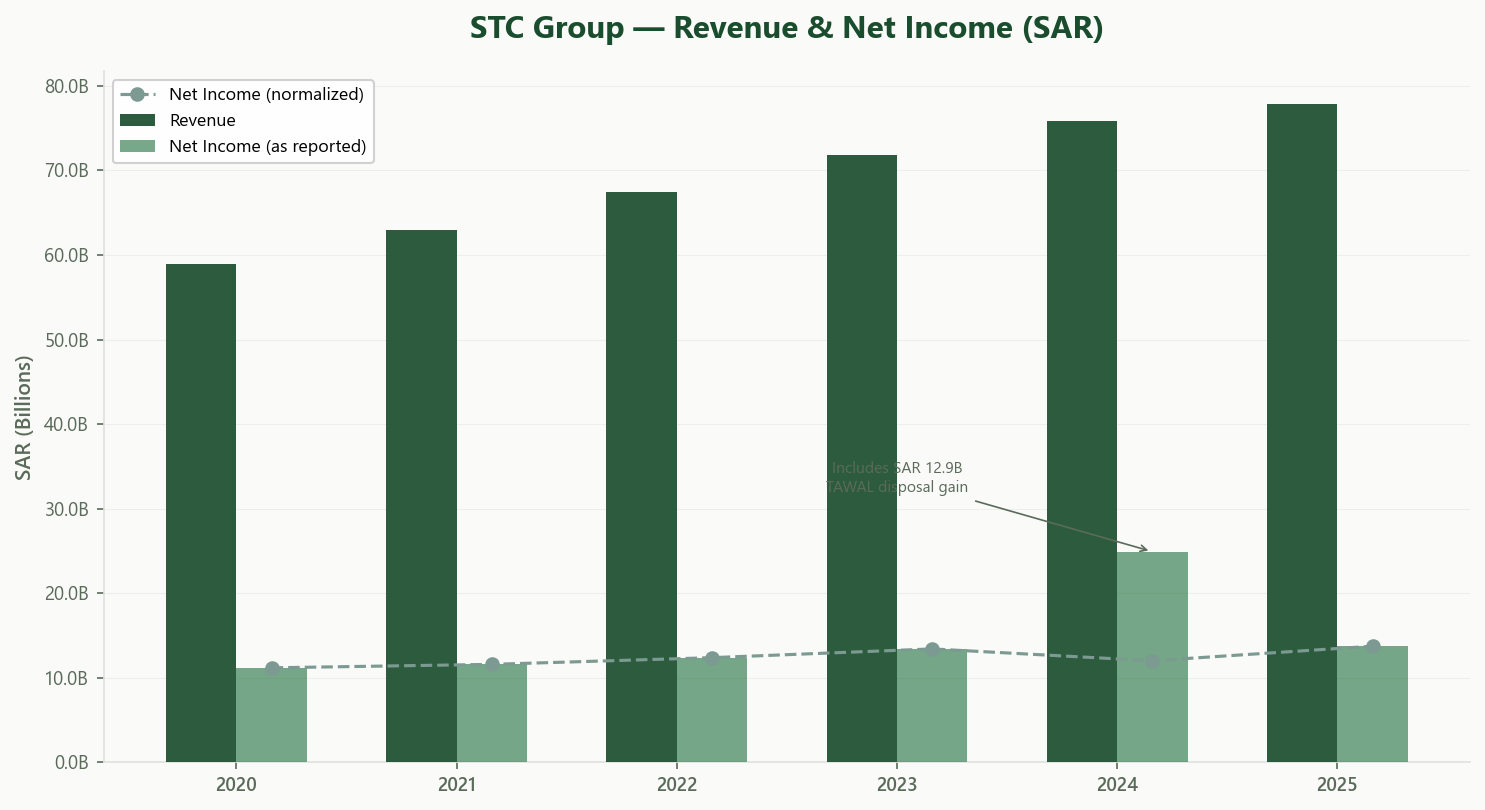

stc's top line has been on a steady climb. Revenue grew from SAR 59 billion in 2020 to SAR 77.8 billion in 2025, a compound annual growth rate of roughly 5.7%.

The net income line, however, requires closer reading.

In 2024, stc reported net income of SAR 24.9 billion. That number included a SAR 12.9 billion one-time gain from selling a controlling stake in its telecom towers subsidiary, TAWAL, to a PIF subsidiary. Strip that out, and 2024 core earnings were around SAR 12 billion.

In 2025, reported net income was SAR 15.1 billion — but this too includes roughly SAR 1.4 billion in net non-recurring items (primarily a SAR 1.3 billion reversal of prior-year zakat provisions). Normalized earnings come closer to SAR 13.7 billion.

The press release highlights "12.5% net profit growth after excluding non-recurring items." That's comparing a cleaned-up 2024 base against a cleaned-up 2025 figure. The normalized trajectory is positive — but it's the kind of steady, low-double-digit growth that won't grab headlines on its own. The headline grabs came from the one-off items.

Profitability & Value Creation: Where stc Truly Shines

This is where stc's financial profile stands out.

stc's Return on Invested Capital (ROIC) stands at approximately 19%. Its Weighted Average Cost of Capital (WACC) — an estimated figure based on the risk-free rate, equity risk premium, and capital structure — typically falls in the 7–9% range for a company like stc. That implies a value creation spread of roughly 10–12 percentage points.

In practical terms, stc consistently earns well above what investors require as a minimum return. Even at the upper end of the WACC range, the spread is comfortably positive. That's a strong indicator of genuine value creation, and it's one of the more compelling aspects of stc's financial profile.

This matters more than headline profits. A company can report high earnings but still destroy value if its returns don't exceed its cost of capital. stc passes this test convincingly, year after year.

Operating margins remain stable around 17–18%, supported by the scale of the telecom business and growing contributions from digital subsidiaries like Solutions, stc Bank, and Center3.

Cash Flow & Dividends

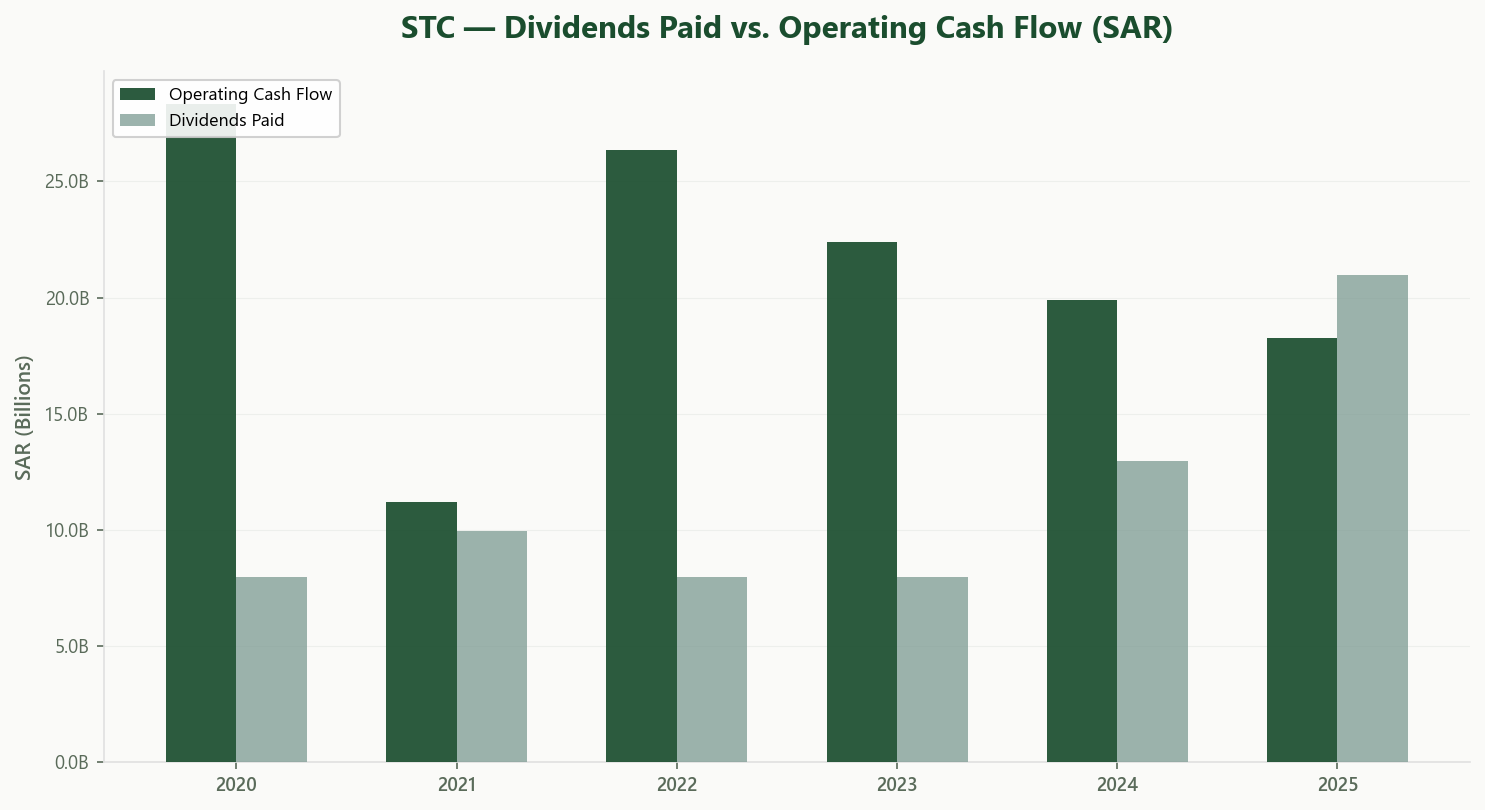

stc generated SAR 18.3 billion in operating cash flow in 2025 and paid out SAR 21.4 billion in dividends — meaning payouts exceeded cash generation by about SAR 3.1 billion.

This was manageable because stc entered 2025 with a substantial cash balance of SAR 30.8 billion (partly from the SAR 8.7 billion TAWAL sale proceeds). By year-end, that balance had settled to SAR 15.1 billion — still healthy.

To understand the current ~10% dividend yield, it helps to look at the trend. From 2020 to 2023, stc paid roughly SAR 8 billion per year in dividends — steady and well-covered by cash flow. In 2024, that rose to SAR 13 billion. In 2025, it reached SAR 21.4 billion, boosted by a special distribution tied to the TAWAL proceeds.

Going forward, stc has committed to a minimum quarterly dividend of SAR 0.55 per share through Q3 2027. With ~5 billion shares outstanding, that's a floor of SAR 11 billion annually — comfortably within operating cash generation. If dividends normalize to that level, the forward yield at current prices would settle around 5–6%, which is still attractive for a company with stc's capital efficiency. The current 10% reflects an unusually large 2025 payout rather than a new baseline.

Stock Performance & Valuation Snapshot

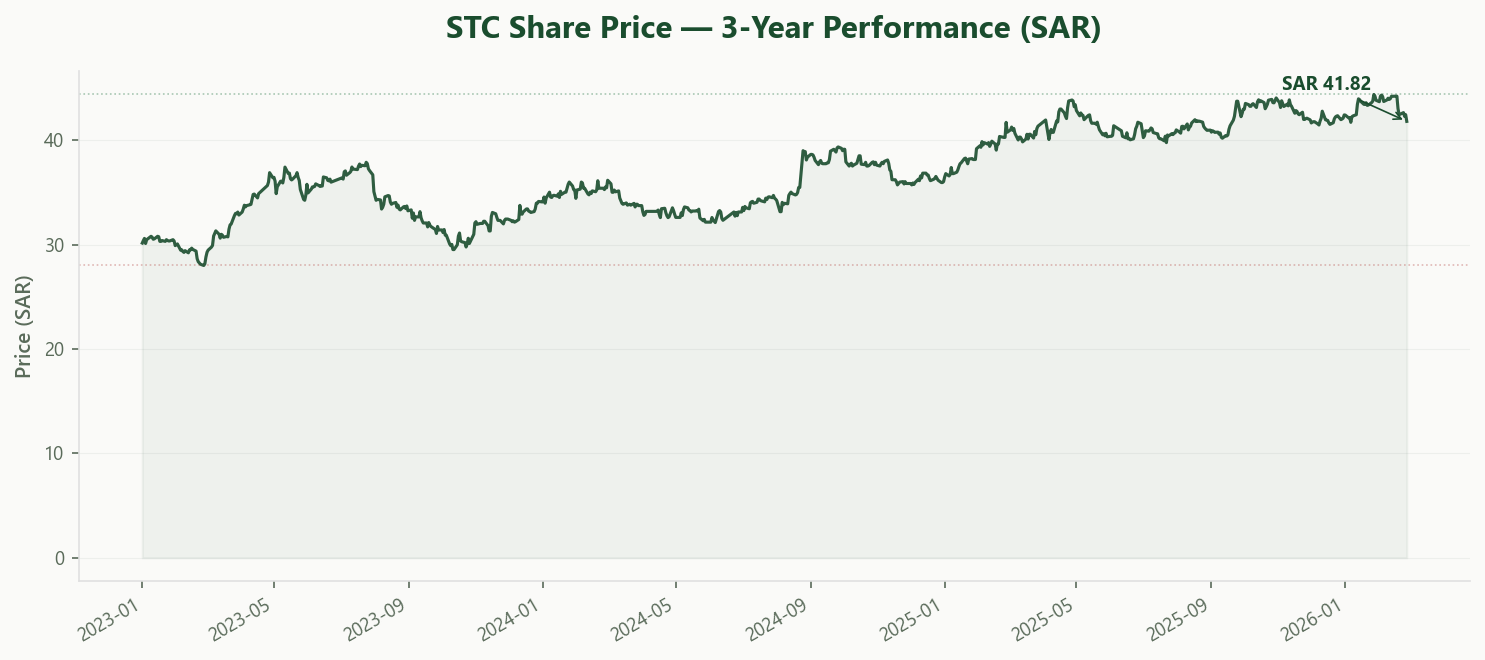

stc currently trades at SAR 41.82, giving it a market capitalization of approximately SAR 209 billion. Over the past three years, the stock has been relatively flat, returning about 14% or roughly 4.5% annualized (excluding dividends).

At the fundamental level, the valuation looks reasonable:

The combination of high returns on capital, conservative leverage, and a generous dividend makes stc one of the stronger profiles in the Saudi market from a pure financial quality standpoint.

Takeaway

stc group is a fundamentally strong company. Its ROIC is well above its cost of capital, its balance sheet is conservative, and its revenue growth has been consistent for years.

The 2025 annual report adds useful context to the headline numbers. Net income, while growing, is shaped by non-recurring items in both 2024 and 2025. The dividend payout was elevated due to TAWAL-related proceeds. Understanding these details gives a more complete picture of the business beyond the press release summary.

For investors evaluating stc, the underlying quality of the business is clear. The question is whether the current valuation and dividend expectations fully reflect the normalized earnings trajectory and the structural dynamics of the ownership.

Explore STC's Full Profile

Usool Research tracks stc's financials, governance disclosures, valuation metrics, and more — structured and updated from every filing. See the full picture for yourself.

Sign up free and explore the data.

Start Exploring →Look for value. Cut through the noise.

Disclaimer: This article is for informational and educational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any securities. The author and Usool Research may hold positions in securities discussed. Usool Research is not a licensed investment advisor. All data sourced from publicly available filings and the Usool Research platform.