Thob Al Aseel Annual Report 2025:

Flat Revenue, Expanding Margins

Thob Al Aseel is the leading thobe and fabric retailer in Saudi Arabia. Revenue has been stable for five years, but net income rose 19% in 2025 on margin expansion alone. The company carries zero bank debt and SAR 284 million in cash. A closer look at the business model, capital efficiency, and what the valuation implies.

What Does Al Aseel Do?

Thob Al Aseel Company (Tadawul: 4012) is a Saudi joint-stock company engaged in the import, export, wholesale, and retail of fabrics and ready-made thobes. The business operates through 26 branches across Saudi Arabia under the "Al Aseel" and "Al Jedaie" brands.

Revenue comes from two core segments: Thobes (SAR 381 million, 72% of revenue) and Fabrics (SAR 132 million, 25%). In 2025, the company launched a new segment, Fashions (SAR 15 million, 3%), through a 45% joint venture with Jadeh Al Hareer Trading Company, a Turkish fashion entity. All revenue is generated within Saudi Arabia.

The company has 400 million shares outstanding (SAR 10 par value). Its subsidiaries include Al Jedaie Fabrics Company, Qiwa Al Aseel Contracting, and Aseelah Trade Company. The Group is Saudi-owned and subject to zakat.

Revenue & Earnings

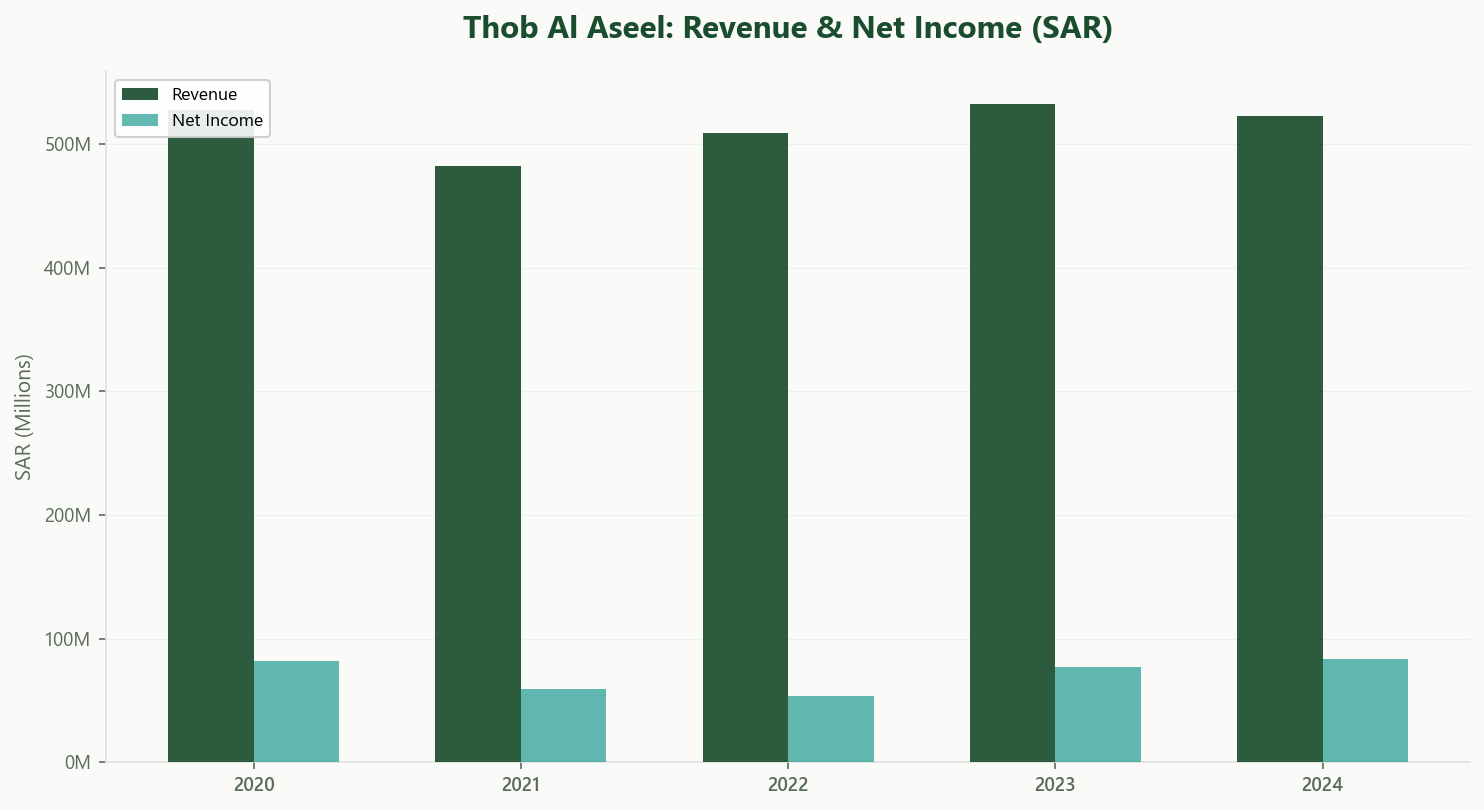

Revenue has hovered between SAR 480 million and SAR 530 million since 2021. In 2025, it came in at SAR 528 million, essentially flat compared to SAR 522 million in 2024. This is not a growth story. Revenue has compounded at roughly 2% annually over five years.

Net income tells a different story. Earnings dipped to SAR 53 million in 2022, then recovered steadily: SAR 77 million in 2023, SAR 84 million in 2024, and SAR 100 million in 2025, a 19% year-over-year increase. The improvement came not from revenue growth but from margin expansion.

EBIT rose from SAR 97 million in 2024 to SAR 113 million in 2025. The operating margin expanded from 18.6% to 21.4%. Gross margins improved as the company managed its input costs and inventory mix more effectively.

Finance costs remained low at SAR 4 million, reflecting the company’s minimal leverage. Zakat expense was SAR 13 million. There were no major non-recurring items in 2025 beyond a SAR 11.6 million reversal of prior impairment losses on trade receivables and a SAR 2 million provision for legal liabilities.

Profitability & Value Creation

Return on Invested Capital (ROIC) stands at approximately 20.9%, against an estimated WACC in the 6 to 8% range. That implies a value creation spread of roughly 13 to 15 percentage points.

The business requires very little capital to operate: no bank debt, minimal lease liabilities (SAR 33 million total), and capex of just SAR 8 million per year. This is a capital-light retailer that generates strong returns on a clean balance sheet.

The operating margin of 21.4% is strong for a specialty retailer. The Thobe segment reported profit of SAR 82 million on SAR 381 million revenue (21.6% margin), while Fabrics contributed SAR 28 million on SAR 132 million revenue (20.9% margin). The new Fashions segment posted a SAR 10 million loss on SAR 15 million revenue, reflecting startup costs from the Jadeh Al Hareer joint venture.

On the governance side, related-party transactions are modest. Lease payments to shareholders totaled SAR 1.8 million and lease liabilities due to shareholders were SAR 2.6 million. Key management compensation increased to SAR 7.7 million from SAR 4.0 million in 2024. The company also provided SAR 3.2 million in payments on behalf of Jadeh Al Hareer (the fashion JV associate), recorded as a receivable.

Cash Flow & Balance Sheet

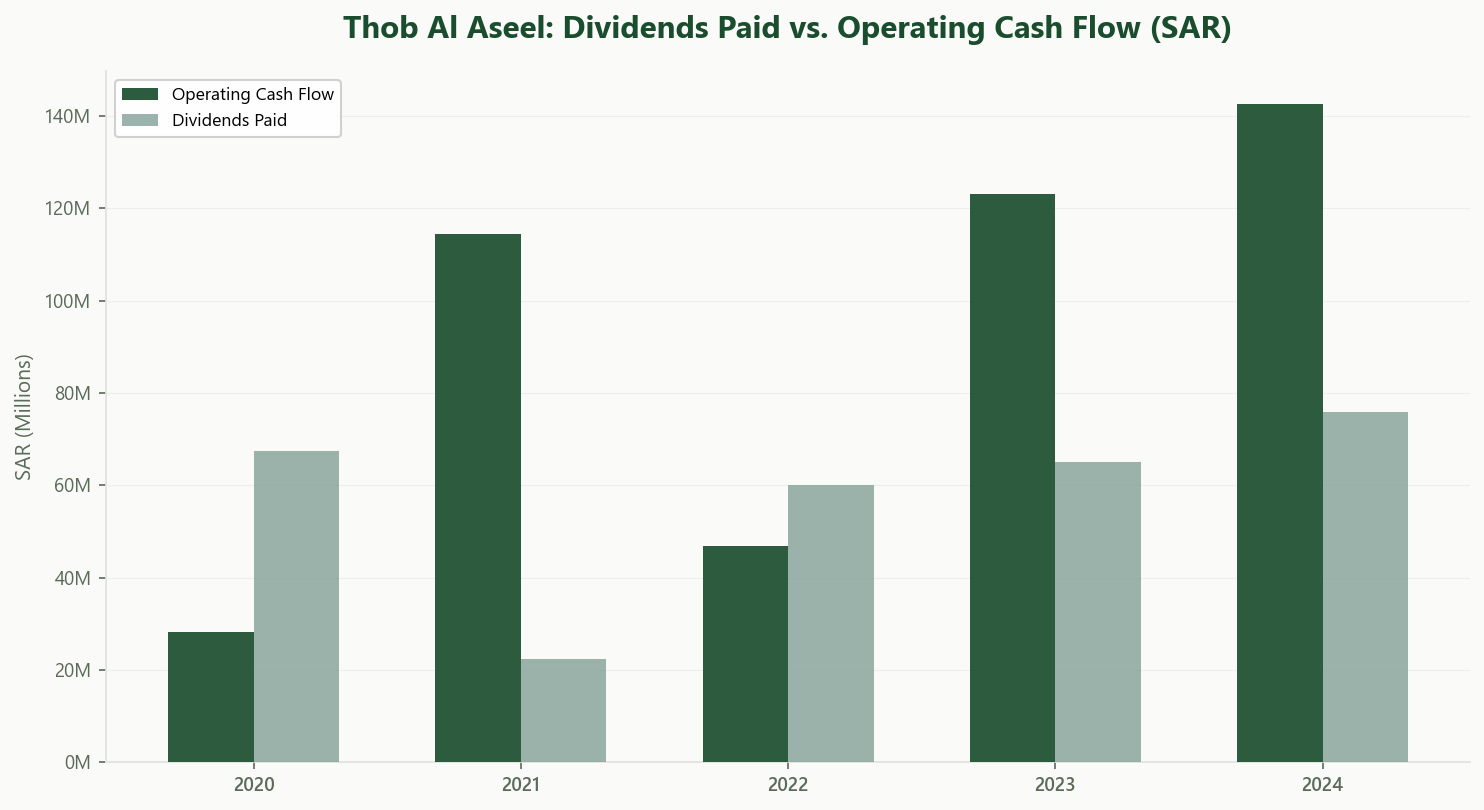

Operating cash flow reached SAR 211 million in 2025, up from SAR 143 million in 2024 and SAR 123 million in 2023. The improvement was partly driven by a SAR 68 million reduction in trade receivables (from SAR 174 million to SAR 106 million) and improved working capital management.

With negligible capex, nearly all operating cash flow converts to free cash flow—approximately SAR 203 million in 2025.

Dividends have grown from SAR 60 million in 2022 to SAR 80 million in 2025. At 80% of net income, the payout ratio is generous but well covered by operating cash flow. The Board distributed dividends in two tranches of SAR 40 million each during 2025.

The balance sheet carries no bank debt. Cash and equivalents stood at SAR 284 million at year-end, up from SAR 190 million a year earlier. Total lease liabilities are SAR 33 million (SAR 21 million current, SAR 12 million non-current). Total shareholder equity is SAR 611 million. Inventory of SAR 263 million (35% of total assets) is the largest single asset.

The company transferred SAR 77 million to statutory reserves in 2024 as part of regulatory compliance, but this had no impact on total equity or cash.

Valuation & What It Implies

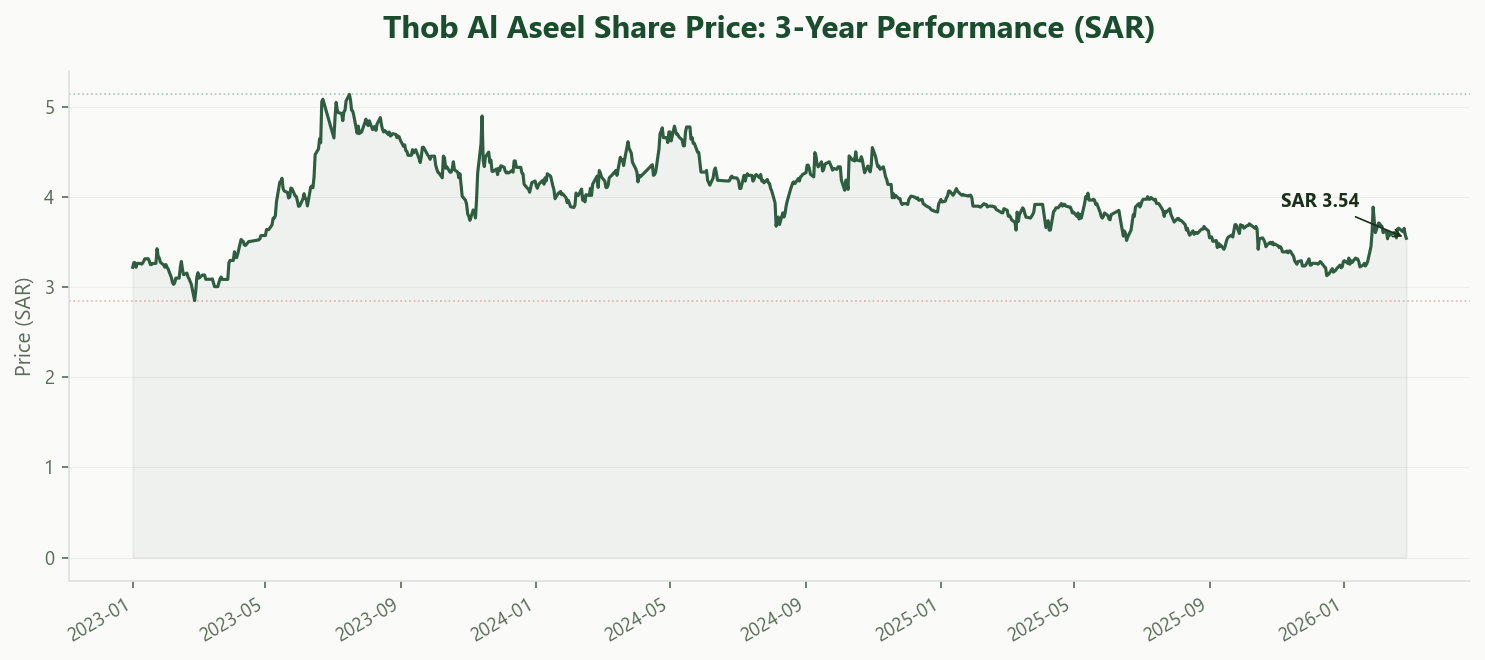

At the recent share price of SAR 3.51:

With 400 million shares outstanding, the market capitalization is approximately SAR 1.40 billion. On trailing 2025 net income of SAR 100 million, the P/E is about 14x. For a business with stable revenue, expanding margins, no debt, and ROIC above 20%, that multiple is not expensive by Tadawul standards.

Enterprise value is straightforward. Adding SAR 33 million in lease liabilities and subtracting SAR 284 million in cash gives an EV of roughly SAR 1.15 billion. Against EBITDA of approximately SAR 119 million (EBIT of SAR 113 million plus SAR 5.7 million in depreciation), the EV/EBITDA is about 9.7x.

The bull case: the business generates strong free cash flow, carries no debt, pays a growing dividend, and has optionality from the fashion JV. If the Fashions segment scales, it could add a growth layer to an otherwise steady-state business.

The bear case: revenue has been flat for years. The company operates in a mature market with limited room for store expansion. The Fashions segment is loss-making and the JV partner is Turkish, introducing operational and currency risk. At 14x earnings, the stock is reasonably priced, but it needs the margin improvement to hold or the Fashions bet to pay off.

Takeaway

Thob Al Aseel’s core business is in solid shape. Revenue is flat, but margins are expanding. The balance sheet carries SAR 284 million in cash and zero debt. ROIC of approximately 21% against an estimated WACC in the 6 to 8% range means the business earns well above its cost of capital. The dividend has grown every year.

The 2025 annual report shows a company that improved its earnings by 19% through better margins, not aggressive expansion. The key risk is the new Fashions segment, which lost SAR 10 million in its first year through the Jadeh Al Hareer joint venture. If management contains those losses and the core thobe and fabric business holds its margins, the capital return characteristics remain attractive.

At 14x trailing earnings and roughly 10x EV/EBITDA, the market is not paying a premium for this business. Whether it should depends on whether revenue growth returns or whether margin expansion alone is enough to sustain the earnings trajectory.

Explore Al Aseel's Full Profile

Usool Research tracks Al Aseel's financials, governance disclosures, valuation metrics, and more. Structured and updated from every filing.

Sign up free and explore the data.

Start Exploring →Look for value. Cut through the noise.

Disclaimer: This article is for informational and educational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any securities. The author and Usool Research may hold positions in securities discussed. Usool Research is not a licensed investment advisor. All data sourced from publicly available filings and the Usool Research platform.