Cenomi Retail (4240) Annual Report 2025: A Significant Turnaround and Ownership Shift

Cenomi Retail is navigating a major structural turnaround in the Saudi market. Burdened by debt and negative operating margins, the company saw a pivotal shift in 2025 as Al Futtaim Retail Company acquired a majority stake. With revenue at SAR 5.10 billion but net income declining to a SAR 496.7 million loss, the focus is squarely on restructuring, asset rationalization, and managing its leverage.

What Does Cenomi Retail Do?

AFG International Company (Tadawul: 4240), formerly known as Fawaz Abdulaziz Al Hokair & Co. (Cenomi Retail), is a leading multi-brand franchise operator headquartered in Saudi Arabia. The group manages a broad portfolio of international brands across fashion, electronics, food & beverage, and entertainment. In addition to its domestic operations, the company operates in Egypt, Jordan, Kazakhstan, Azerbaijan, Georgia, Armenia, and Uzbekistan.

In 2025, Fashion Retail remained the dominant segment, contributing SAR 4.28 billion (84% of revenue), but operating at a significant segment-level loss. Electronics added SAR 494.8 million, while Food and Beverages generated SAR 323.3 million. Geographically, Saudi Arabia accounts for 69% of revenue and 90% of total assets, with international operations contributing the remaining 31%.

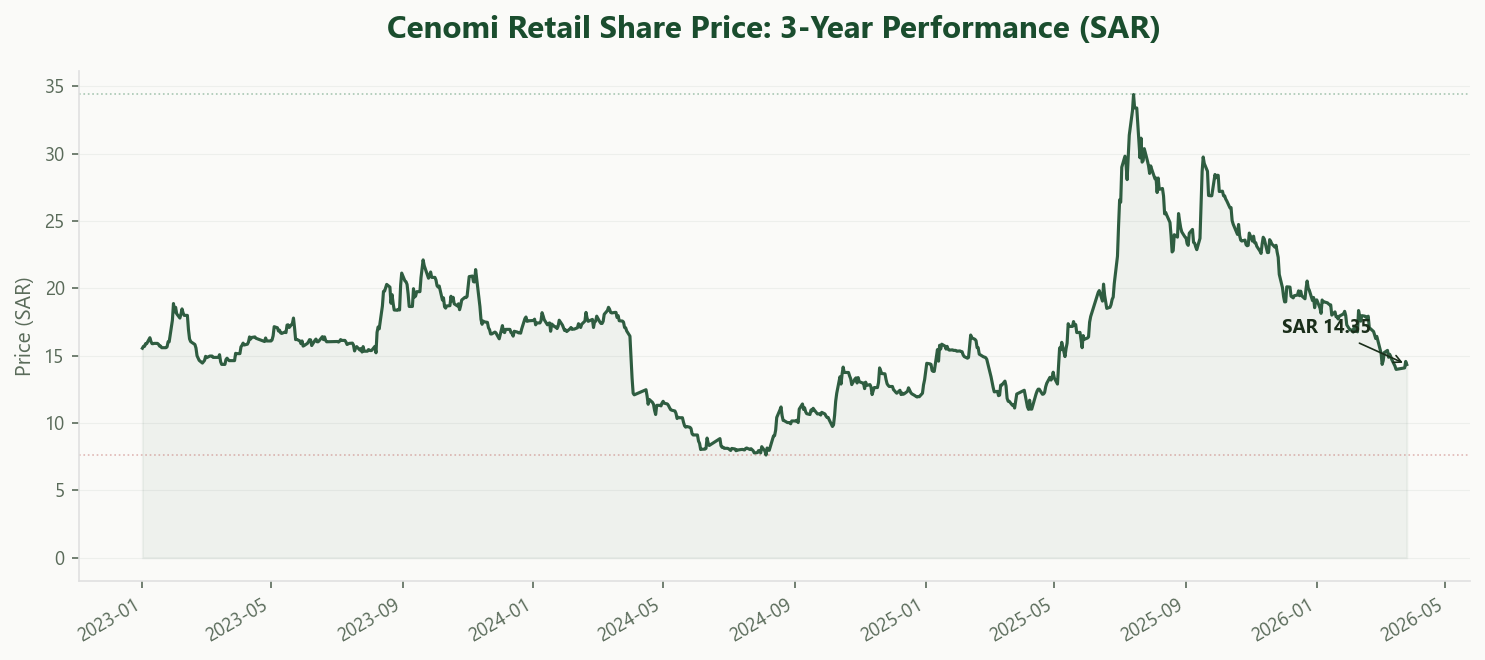

The company has 114.7 million shares outstanding. In a pivotal transaction on September 15, 2025, the founding shareholders sold a 49.95% stake to Al Futtaim Retail Company for SAR 2.52 billion (SAR 44 per share), marking a complete shift in control to a new ultimate parent entity based in the UAE.

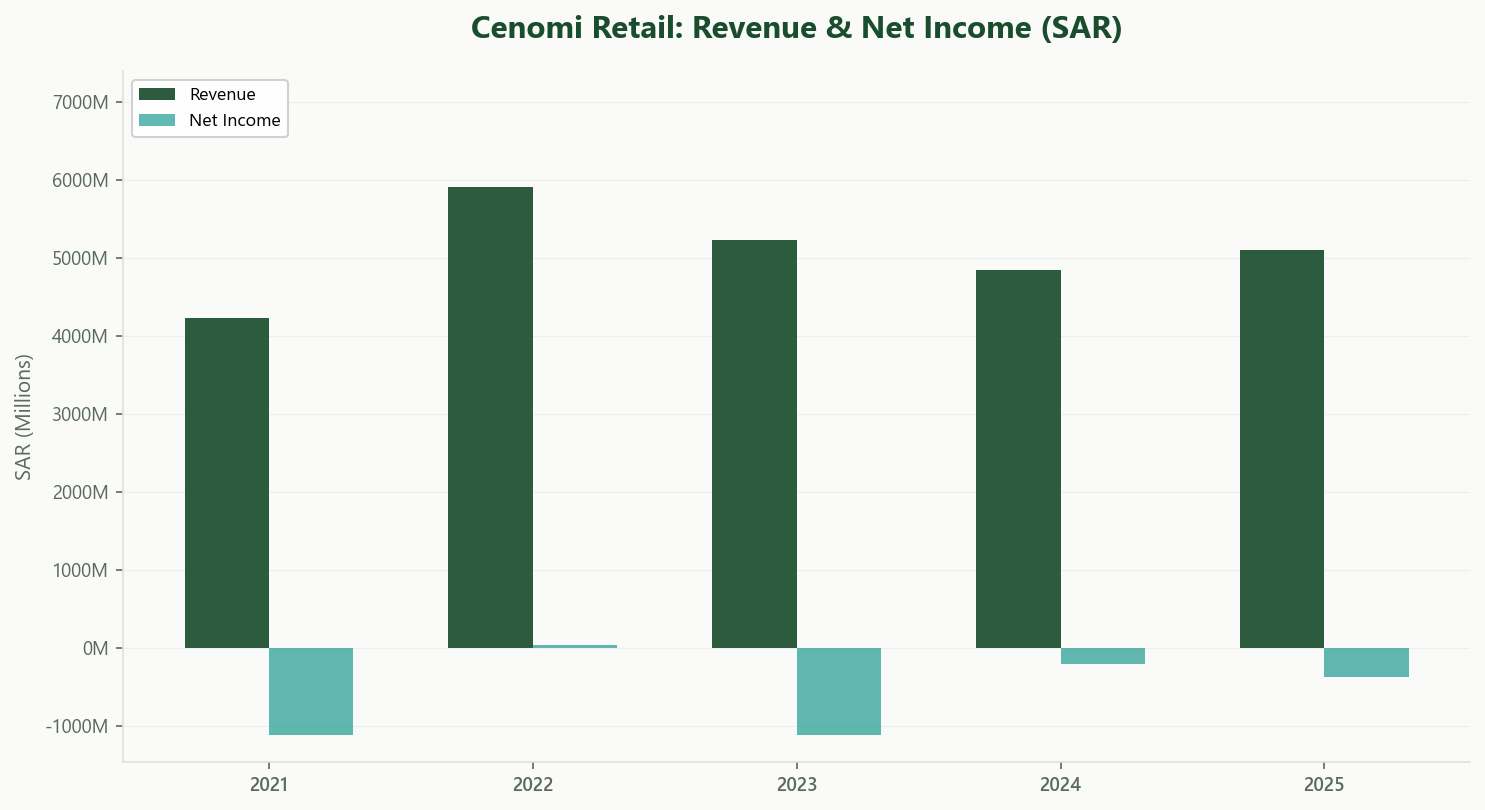

Revenue & Earnings: Revenue Holds, Losses Deepen

Revenue showed modest stabilization in 2025, growing 5% to SAR 5.10 billion from SAR 4.84 billion. It remains below historical peaks, reflecting a deliberate strategy of pruning the portfolio and exiting structurally unprofitable brand partnerships.

Profitability challenges persist. The net loss widened to SAR 496.7 million (EPS of SAR -4.40), from SAR 197.4 million in 2024. The deterioration reflects rising operating costs, non-cash impairment charges, and a heavy finance burden.

EBIT fell to SAR -90.5 million, reversing from SAR 229.1 million in 2024. The swing underscores the difficulty of operating a high-fixed-cost retail network amidst brand rationalization and competitive discounting.

Non-recurring items weighed on earnings: a SAR 120 million impairment on goodwill (Nesk subsidiary), SAR 57.9 million in property write-offs, and a SAR 65.3 million inventory provision. These were partially offset by a SAR 19 million gain on brand disposals.

Profitability & Value Creation

The company is experiencing a decline in value creation. Five-year average ROIC sits at roughly -3.7% against a WACC in the 6 to 8% range. The spread is negative. The turnaround is reliant on external refinancing rather than internal cash generation.

Capex for 2025: SAR 105.1 million. Depreciation and amortization: SAR 136.9 million. Capital expenditure intentionally trails D&A, signaling a shrinking physical footprint as the company focuses on rationalization over growth.

Segment profitability tells the story. Fashion Retail posted a SAR 420.1 million loss. Electronics produced a modest SAR 8.7 million profit. Food and Beverages lost SAR 37.1 million. The core engine is misaligned with its cost structure.

Governance warrants monitoring. Following the 49.95% acquisition by Al Futtaim, the group entered into substantial related-party financing. The intermediate parent affiliate injected a SAR 1.35 billion shareholder loan at 3-month SAIBOR plus 3.6%, with an equity conversion option. A new SAR 1.6 billion bank facility was secured via a corporate guarantee from Al Futtaim Private Company. Prior to the acquisition, the group executed SAR 183.2 million in related-party rental transactions with Arabian Centers and adjusted SAR 14.9 million in land values to settle related-party rental liabilities. The pattern highlights a capital structure reliant on continued related-party support for solvency.

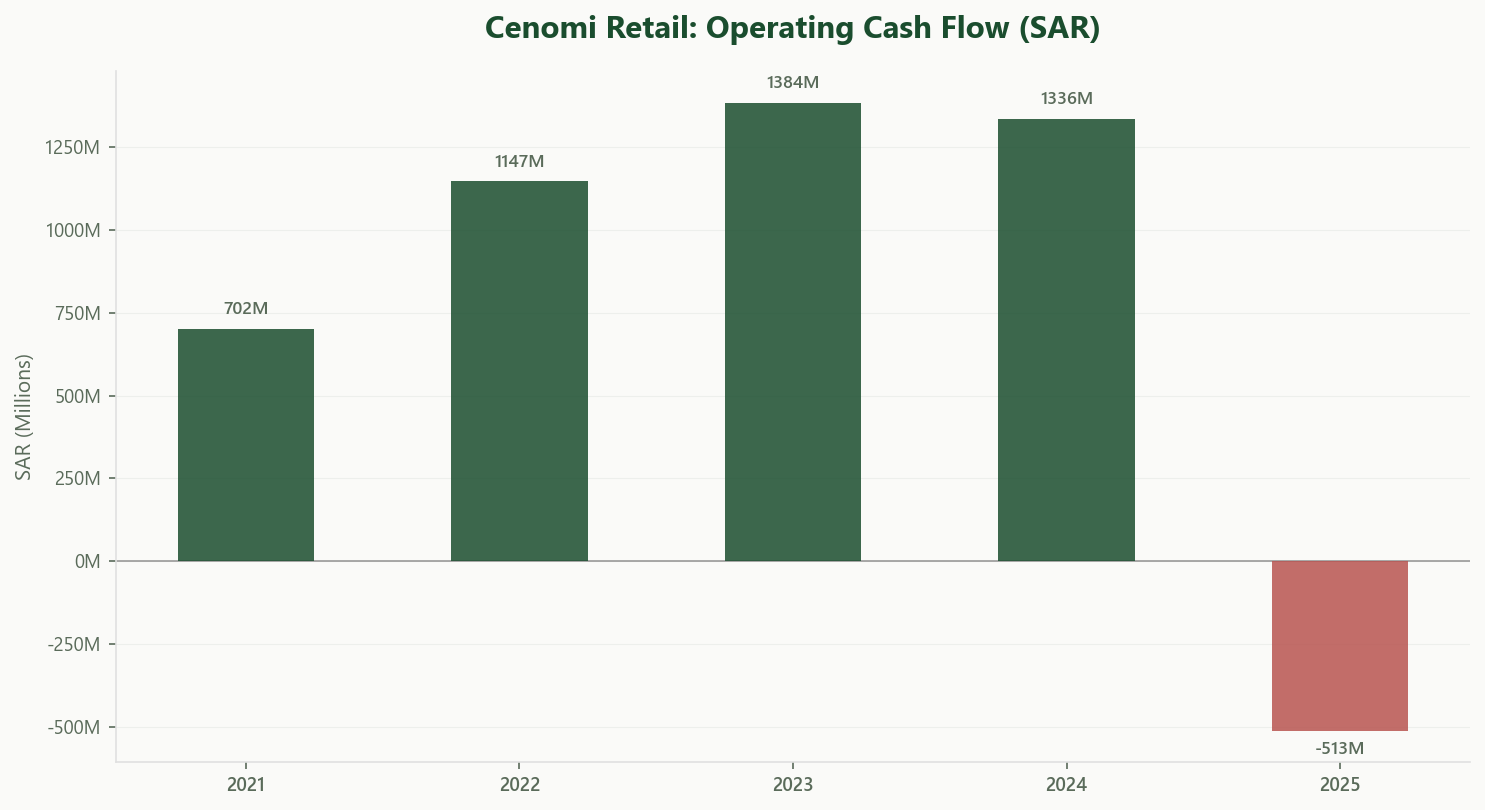

Cash Flow & Balance Sheet

Cash generation deteriorated in 2025. Operating cash flow swung to an outflow of SAR 512.7 million, from a positive SAR 1.33 billion in 2024. The reversal reflects operating losses, interest costs, and working capital requirements.

Free cash flow is negative. The company depends on external financing to operate. No dividends were paid and no shares were repurchased.

The balance sheet is highly levered with a structural equity deficit. Total shareholder equity: negative SAR 1.46 billion. The current portion of long-term loans stands at SAR 1.41 billion, a near-term liquidity burden mitigated only by the recent refinancing.

Long-term obligations are substantial: SAR 1.25 billion in finance leases and SAR 1.57 billion in non-current derivative liabilities. Interest service totaled SAR 289.7 million in 2025.

Cash sits at SAR 244 million against current liabilities exceeding current assets. The capital structure depends on the Al Futtaim debt restructuring framework.

Valuation & What It Implies

At the acquisition anchor price of SAR 44.00 per share:

With 114.7 million shares outstanding, market capitalization equates to roughly SAR 5.05 billion. Pricing a company with negative equity, negative earnings, and negative operating cash flow requires a turnaround framework, not conventional earnings multiples.

Enterprise value is dominated by debt. Adding short-term borrowings, lease liabilities, and non-current obligations, EV stands well above equity value. Unlike profitable retail peers such as Jarir (4190), Alsaif Gallery (4192), and Extra (4003), EV/EBITDA is not meaningful given negative operating profitability.

The bull case: Al Futtaim’s operational expertise and capitalization capability drive a successful turnaround. If the newly secured SAR 1.6 billion facility and the SAR 1.35 billion shareholder loan provide enough runway to rationalize the brand portfolio and renegotiate leases, the company may eventually return to profitability. The equity conversion option on the shareholder loan also provides an avenue to recapitalize the balance sheet.

The bear case: The stock remains fundamentally challenged. With ROIC below WACC and negative free cash flow, the company is depleting capital. If the fashion segment cannot reverse its SAR 420 million loss, the debt burden will eventually outpace the remaining enterprise value, diluting minority shareholders if the debt conversion is triggered.

Takeaway

Cenomi Retail is undergoing a major structural overhaul. Revenue stands at SAR 5.10 billion, but operating margins and cash flow are negative, and shareholder equity is below zero. The business model is being rebuilt under new ownership.

The heavy reliance on related-party financing—including a SAR 1.35 billion shareholder loan with a 3-month SAIBOR + 3.6% rate—is worth monitoring. It serves as a necessary lifeline but introduces dilution risk and shifts significant control to the new parent entity.

At an implied market cap of SAR 5 billion, the market is pricing a successful turnaround by Al Futtaim. The question: is the runway provided by the new debt structure enough to fix an operationally unprofitable core?

Explore Cenomi Retail’s Full Profile

Usool Research tracks Cenomi Retail’s financials, governance disclosures, valuation metrics, and more. Structured and updated from every filing.

Sign up free and explore the data.

Start Exploring →Look for value. Cut through the noise.

Disclaimer: This article is for informational and educational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy or sell any securities. The author and Usool Research may hold positions in securities discussed. Usool Research is not a licensed investment advisor. All data sourced from publicly available filings and the Usool Research platform.